Breaking Down the Impact of AI on Equipment Financing in 2026

Introduction

The equipment financing landscape is undergoing its most significant transformation in decades. Artificial intelligence has moved from experimental pilot programs to production-scale deployment, fundamentally reshaping how businesses acquire the machinery, technology, and infrastructure they need to compete. In 2026, the $1.3 trillion equipment financing industry stands at a pivotal crosspoint where intelligent automation meets unprecedented demand for flexible, rapid, and accessible capital solutions.

The numbers tell a compelling story. Credit approvals have reached historic highs of 78%, while delinquency rates remain remarkably stable at just 2%. Businesses are now financing more than three-quarters of their equipment and software purchases instead of buying them outright. Behind these strong metrics lies a technological revolution where machine learning algorithms, natural language processing, and predictive analytics are replacing weeks of manual underwriting with decisions delivered in hours or even minutes.

This comprehensive analysis examines how AI is reshaping equipment financing across five critical dimensions, from underwriting and risk assessment to customer experience and regulatory compliance. Whether you are a business owner seeking equipment capital or a financial professional navigating this evolving landscape, understanding these changes is essential for making informed decisions in the year ahead.

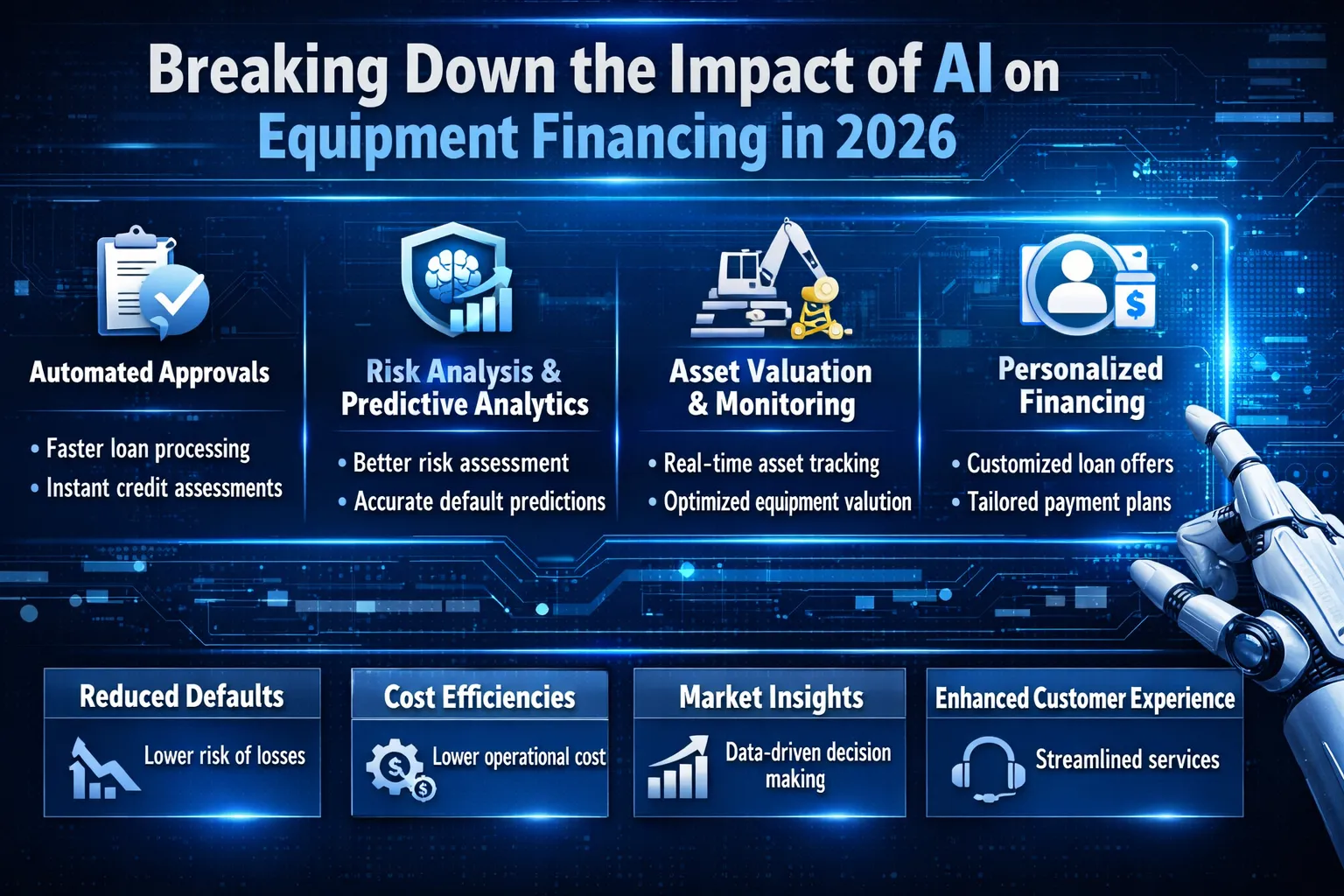

The AI Revolution in Equipment Underwriting

Traditional equipment financing approvals once required extensive documentation review, manual credit analysis, and weeks of back-and-forth communication between lenders and borrowers. This process has been fundamentally transformed by artificial intelligence systems that can evaluate applications with unprecedented speed and accuracy.

Modern AI-powered lending platforms analyze hundreds of data points beyond conventional credit scores. These systems examine real-time cash flow patterns, industry performance benchmarks, equipment utilization rates, and predictive business health indicators to create comprehensive borrower profiles. The result is a dramatic acceleration in decision-making that benefits both lenders and borrowers alike.

Some AI underwriting providers report approval rate increases of 18 to 32 percent among lenders, alongside bad-debt reductions of more than 50 percent. These improvements stem from the technology’s ability to identify creditworthy borrowers that traditional scoring models would miss, particularly in specialized industries with unique financial characteristics.

The shift from traditional automated underwriting systems to advanced AI represents an evolution rather than revolution, balancing continuity with transformative change. Machine learning has been a component of lending for decades, powering credit scores and automated decision engines. However, today’s AI brings far more complex models capable of processing unstructured data, understanding context, and adapting to changing market conditions.

For business owners, this technological shift translates to faster access to capital when opportunities arise. Whether responding to unexpected equipment failures or capitalizing on time-sensitive expansion opportunities, AI-driven approvals provide the speed necessary to maintain competitive advantage in rapidly evolving markets.

Enhanced Risk Assessment Through Machine Learning

Risk assessment represents one of the most profound areas where AI is transforming equipment financing in 2026. Conventional credit evaluation relied heavily on static scores and limited historical data points. Modern machine learning models process thousands of variables simultaneously, capturing nuances that human underwriters might overlook.

AI systems now evaluate how income flows vary over time, how frequently businesses utilize overdraft facilities, how they manage multiple accounts, and whether their financial behavior shows improvement or deterioration. This dynamic assessment provides lenders with a richer picture of creditworthiness that static ratings simply cannot match.

The technology proves particularly valuable for assessing complex financial scenarios common in equipment financing. A construction company seeking heavy machinery financing or a medical practice acquiring diagnostic equipment presents challenges that do not fit neatly into traditional underwriting frameworks. AI systems can holistically evaluate these specialized situations by considering industry-specific risk factors that matter for accurate assessment.

Equipment-specific considerations add another dimension to AI risk modeling. Modern platforms now incorporate asset depreciation curves, workload patterns, and vendor technology roadmaps into their assessments. This proves especially important for AI infrastructure financing, where assets like GPU clusters and specialized hardware depreciate faster than traditional equipment.

Fraud detection capabilities have also advanced significantly. AI can analyze borrower data in real time, identifying patterns and anomalies that may indicate fraudulent activity. These systems flag suspicious applications automatically, allowing lenders to investigate and prevent problems before they materialize. Mortgage fraud attempts increased by more than one-third between 2022 and 2023, making robust AI-powered detection essential across all lending categories.

Streamlined Application and Approval Processes

The operational impact of AI on equipment financing extends far beyond underwriting decisions. Artificial intelligence is streamlining every stage of the application process, from initial document submission through final funding.

AI-powered optical character recognition, natural language processing, and image analysis technologies can automate up to 90 percent of manual loan application processing tasks. This includes document verification, data entry, and borrower communication that previously consumed significant staff time and resources. The collective effect is dramatic reduction in cost-per-loan and substantial improvements in operational scalability.

Lenders can now process higher application volumes without proportional increases in staff. Human underwriters are freed from tedious data transcription to focus on complex, high-touch customer relationships and strategic decision-making. This transformation converts underwriters from data processors into skilled financial advisors who add genuine value to the lending relationship.

Point-of-sale financing embedded directly into equipment purchasing processes has become standard practice in 2026. Rather than separately arranging financing through external lenders, businesses can complete entire equipment acquisitions through unified platforms offered by dealers and manufacturers. This integration dramatically simplifies purchasing, reduces transaction friction, and accelerates acquisition timelines.

Businesses now receive instant financing decisions during equipment selection conversations, enabling immediate commitment to purchases without delays for separate financing arrangements. These embedded financing platforms leverage the same AI-driven underwriting technologies, providing rapid decisions while maintaining appropriate credit standards.

Expanding Access to Equipment Capital

One of the most significant impacts of AI on equipment financing involves expanding access to capital for businesses that traditional models underserved. More sophisticated machine learning models can identify creditworthy borrowers who conventional scoring metrics would have missed, particularly in underserved markets and specialized industries.

This expansion matters enormously for agricultural lending, small business financing, and specific sectors like healthcare practices, restaurants, and manufacturing operations. These businesses frequently exhibit unique cash flow patterns and risk factors that do not align neatly with standard credit models. AI systems can assess them more fairly by accounting for industry-specific factors and analyzing diverse data sources.

New businesses can reduce their initial communication and equipment costs by up to 90 percent by choosing financing over outright purchase, and AI is making these options accessible to a broader range of companies. Many businesses that were previously rejected by traditional banks can now qualify through fintech lenders whose AI systems evaluate more than just credit scores to create fuller pictures of how businesses actually operate.

Alternative data sources play a crucial role in this democratization of access. AI systems can analyze payment histories with vendors, business social media profiles, online review patterns, and industry performance trends to supplement traditional credit information. For borrowers with limited credit histories or unconventional financial situations, this comprehensive analysis opens doors that remained closed under legacy evaluation methods.

The technology also enables micro-lending solutions and specialized financing programs tailored to specific business needs. Equipment-as-a-Service models, subscription-based arrangements, and usage-driven financing structures all benefit from AI’s ability to assess and monitor borrower performance in real time.

Regulatory Compliance and Transparency Challenges

As AI becomes central to equipment financing decisions, regulatory frameworks are evolving to address new risks and responsibilities. The European Union’s AI framework classifies credit scoring and underwriting as high-risk uses of artificial intelligence, carrying specific obligations around data quality, documentation, testing, human oversight, and transparency.

Lenders must demonstrate how they manage model risk, assess potential bias, monitor ongoing performance, and provide meaningful information to customers affected by automated decisions. These requirements influence global practice beyond European markets, as international financial institutions tend to harmonize their standards with the strictest applicable regimes.

One of the most pressing concerns involves model explainability. Unlike traditional rules-based systems, many AI and machine learning models function as black boxes, making it challenging for lenders and regulators to understand exactly how input data generates decisions. This opacity can hinder efforts to detect or correct discriminatory practices that might emerge from algorithmic processing.

Another significant risk comes from potential use of proxy variables that indirectly incorporate prohibited characteristics into lending decisions. While AI systems can adapt and learn over time, improving both efficiency and accuracy, financial institutions must remain vigilant in monitoring these evolving patterns. Ongoing oversight, robust documentation, and continuous testing are necessary to ensure models remain fair, transparent, and compliant.

Advanced AI platforms now incorporate explainability features that document exactly how systems reach their conclusions. This includes citation technology linking extracted data points back to source documents, confidence scores indicating reliability of different analysis components, and natural language explanations of how key factors influenced overall risk assessments.

The Future of AI-Driven Equipment Financing

Looking ahead, the trajectory of AI in equipment financing points toward even deeper integration and more sophisticated capabilities. By 2027, the financial industry is expected to invest nearly $97 billion in AI, up from $35 billion in 2023, with lending applications capturing a significant share of this investment.

Autonomous AI agents will increasingly handle routine customer requests, from answering product inquiries to assisting with application troubleshooting. Contemporary AI assistants use natural language processing to understand context and intent, enabling more natural and useful conversations than the frustrating automated systems of previous decades.

Equipment financing will continue adapting to new asset classes and financing needs. AI infrastructure itself has created explosive demand for specialized hardware financing, with platforms requiring technical expertise to evaluate GPU clusters, data center equipment, and rapidly evolving technology assets. Morgan Stanley projects $3 trillion in data center spending through 2029, creating substantial financing opportunities for lenders prepared to serve this market.

The balance between automation and human judgment will remain essential. Research consistently shows that people prefer human interaction for complex financial decisions, highlighting the need for AI to complement rather than replace skilled lending professionals. Successful equipment financing in 2026 and beyond will leverage intelligent automation while preserving the relationships and expertise that borrowers value.

Conclusion

Artificial intelligence has fundamentally transformed equipment financing in 2026, delivering faster approvals, more accurate risk assessment, expanded access to capital, and streamlined operational processes. The technology enables lenders to process applications in hours rather than weeks while achieving better outcomes for both institutions and borrowers.

For businesses seeking equipment capital, these changes translate to unprecedented convenience and opportunity. AI-powered platforms can evaluate applications quickly, identify creditworthy borrowers that traditional models overlook, and deliver financing decisions that match the pace of modern business operations.

The equipment financing landscape will continue evolving as AI capabilities advance and regulatory frameworks mature. Lenders who embrace intelligent automation while maintaining appropriate human oversight will capture the market opportunities that technological transformation creates. Businesses that understand how to leverage AI-enhanced financing will access the equipment they need to grow, compete, and thrive in an increasingly dynamic economic environment.

The question for business owners and financial professionals alike is no longer whether AI will impact equipment financing, but how to position themselves advantageously within this transformed landscape. Those who adapt quickly will find themselves with significant competitive advantages in the years ahead.

{kind=link}

No comment